Introduction

Capital gains tax is a crucial consideration for anyone selling assets like stocks, real estate, or valuable collectibles. In simple terms, capital gains are the profits earned from the sale of an investment or property that has increased in value. While this might sound straightforward, how much you owe in taxes can vary widely depending on factors like how long you held the asset and your income level.

California capital gains tax can be particularly burdensome due to the state’s high income tax rates, unlike the federal government, which distinguishes between short-term and long-term capital gains, California taxes all capital gains as ordinary income. That means even long-term investments can face some of the highest tax rates in the nation.

Planning for capital gains tax is essential, especially in a high-tax state like California. Without a clear strategy, you could be left with a significant tax bill that eats into your hard-earned profits. Smart planning helps you minimize tax liability, take advantage of deductions, and align your investment timeline with tax efficiency.

What Are Capital Gains?

Capital gains refer to the profit made when you sell an asset for more than what you originally paid for it. The difference between the purchase price (known as the “cost basis”) and the sale price is your capital gain. This gain is considered taxable income in the year the asset is sold.

Types of Capital Gains:

- Short-term capital gains apply to assets held for one year or less. These gains are typically taxed at your ordinary income tax rate.

- Long-term capital gains apply to assets held for more than one year. Federally, these gains are taxed at a lower rate than short-term gains, but in California, both are taxed as regular income.

Common Examples of Capital Gains Include:

- Selling real estate for more than its purchase price

- Selling stocks or mutual fund shares that have appreciated

- Selling business assets or ownership shares for a profit

Understanding the type of capital gain you’re dealing with is crucial, as it directly impacts your tax liability and planning strategy.

Understanding Capital Gains

Capital gains are realized when you actually sell the asset and receive the profit. Until that sale happens, any increase in value is considered an unrealized gain, which is not taxable. This distinction matters, especially for investors who prefer to hold onto assets to delay or reduce taxes.

Realized vs. Unrealized Gains:

- Unrealized gains are paper profits, your asset is worth more, but you haven’t sold it.

- Realized gains occur when the asset is sold, and the profit is subject to taxation.

Cost Basis and Gain Calculations:

Your cost basis is what you paid for the asset, including certain fees or commissions. To calculate your capital gain, you subtract your cost basis from the sale price. A higher cost basis results in a lower taxable gain, while a lower cost basis means a larger gain and potentially more tax.

Holding Period and Tax Impact:

The length of time you hold an asset before selling it determines whether it’s taxed as a short-term or long-term gain (federally). While California does not differentiate between the two for tax purposes, the federal government does, so it still plays a role in your overall tax planning.

Federal Capital Gains Tax Rates

Understanding federal capital gains tax rates is essential for effective tax planning, especially if you’re selling investments like stocks, real estate, or collectibles. The IRS categorizes capital gains into short-term and long-term, and each is taxed differently depending on your income bracket.

1. Federal Tax Brackets for Short-Term and Long-Term Gains

- Short-term capital gains apply to assets held for one year or less. These gains are taxed as ordinary income, meaning the tax rate ranges from 10% to 37%, depending on your federal income tax bracket.

- Long-term capital gains apply to assets held for more than one year. The tax rates for 2024 (to be filed in 2025) are more favorable:

- 0% for individuals with taxable income up to $47,025 (single) or $94,050 (married filing jointly)

- 15% for incomes between $47,026 – $518,900 (single) or $94,051 – $583,750 (married filing jointly)

- 20% for incomes above $518,900 (single) or $583,750 (married filing jointly)

- 0% for individuals with taxable income up to $47,025 (single) or $94,050 (married filing jointly)

2. Additional Taxes for High Earners

High-income taxpayers may owe more than just the base capital gains tax. Here are two key considerations:

- Net Investment Income Tax (NIIT): A 3.8% surtax applies to net investment income (including capital gains) for individuals with modified adjusted gross income (MAGI) over:

- $200,000 (single)

- $250,000 (married filing jointly)

- $200,000 (single)

- Alternative Minimum Tax (AMT) Considerations: While long-term capital gains are generally taxed at favorable rates even under AMT, certain preference items (like exercising incentive stock options) may trigger AMT liability, so planning is essential.

3. Special Tax Rate for Collectibles

Not all capital gains qualify for the standard long-term rates. Collectibles, such as art, antiques, and rare coins, are taxed at a maximum rate of 28% for long-term gains. This higher rate can apply even if your regular capital gains rate is lower, so it’s crucial to know how your investments are classified.

How California Taxes Capital Gains?

Unlike federal tax laws, California does not provide preferential tax treatment for long-term capital gains. Whether you’ve held an asset for one year or ten, all capital gains in California are taxed as regular income.

Capital Gains Taxed as Regular Income

California capital gains tax is treated the same as wages, salary, or business income. This means that both short-term and long-term capital gains are subject to the state’s standard income tax rates, which can be among the highest in the nation.

California State Income Tax Brackets Overview (2024)

The 2024 California income tax brackets for single filers have been updated to reflect inflation adjustments. These rates apply to both ordinary income and capital gains, as California taxes capital gains as regular income without preferential rates.

2024 California Income Tax Brackets (Single Filers)

| Taxable Income Range | Tax Rate |

|---|---|

| $0 – $10,756 | 1.00% |

| $10,757 – $25,499 | 2.00% |

| $25,500 – $40,499 | 4.00% |

| $40,500 – $56,999 | 6.00% |

| $57,000 – $71,999 | 8.00% |

| $72,000 – $375,999 | 9.30% |

| $376,000 – $452,499 | 10.30% |

| $452,500 – $750,999 | 11.30% |

| $751,000 – $999,999 | 12.30% |

| $1,000,000 and above | 13.30% |

Note: These brackets are based on the 2024 California Tax Rate Schedules provided by the Franchise Tax Board (FTB). For detailed information and other filing statuses, refer to the official FTB documents.

Additional Resources

- FTB Tax Calculator: Use the FTB Tax Calculator to estimate your tax liability based on your specific income and filing status. Franchise Tax Board

- FTB Tax Tables: For taxable incomes of $100,000 or less, consult the 2024 California Tax Table to determine your tax.

Additionally, California imposes a 1% Mental Health Services Tax on taxable income exceeding $1 million, effectively increasing the top marginal rate to 13.3% for those high earners.

For other the California Income Tax Rate for other filing status visit the Franchise Tax Board site.

Impact on High-Net-Worth Individuals and Investors

California’s treatment of capital gains has a significant impact on high-net-worth individuals, real estate investors, and those selling appreciated assets. With no break for long-term gains, the total tax liability can be substantial. Many investors factor California’s high tax burden into their investment strategies, sometimes even relocating or structuring sales through tax-advantaged entities.

Case Study: Selling a Home in San Leandro, California

Let’s consider a hypothetical example of a homeowner selling their property in San Leandro to understand how California capital gains tax applies at both the federal and state levels.

Example:

- Original Purchase Price (Basis): $600,000

- Capital Improvements: $100,000

- Adjusted Basis: $700,000

- Sale Price: $1,200,000

- Net Capital Gain: $500,000

Now, let’s apply the IRS primary residence exclusion:

- The IRS allows up to $250,000 exclusion for single filers (or $500,000 for joint filers) if the home was used as a primary residence for at least 2 of the past 5 years.

- In this case, the seller is single, so only $250,000 of the gain is excluded.

- Taxable Gain: $250,000

Estimated Tax Liability:

- Federal Long-Term Capital Gains Tax: 15% of $250,000 = $37,500

- Net Investment Income Tax (NIIT): 3.8% of $250,000 = $9,500

- California State Income Tax (San Leandro resident): ~9.3% of $250,000 = $23,250

(California taxes capital gains as regular income; actual rate varies based on income bracket)

Total Estimated Taxes Owed:

$70,250 (Federal + California)

San Leandro tax planning tip: Working with a local San Leandro tax preparer can help residents of San Leandro minimize capital gains tax by leveraging exclusions, adjusting sale timing, and exploring reinvestment options like Opportunity Zones.

California Capital Gains Tax Planning Strategies

Strategic planning can help reduce or defer the taxes you owe on capital gains. Here are several effective methods used by individuals and investors to manage and mitigate their capital gains tax liability:

1. Tax-Loss Harvesting

One of the most common strategies, tax-loss harvesting, involves selling underperforming assets to offset gains. This approach helps manage California capital gains taxes, especially when used in high-income years.

2. Holding Assets Long-Term

Whenever possible, hold investments for more than one year to benefit from lower federal long-term rates. While California capital gains tax is taxed at the same rate as ordinary income, federal savings can still be substantial with long-term holdings.

3. Charitable Contributions & Trust Strategies

Using charitable vehicles can reduce California capital gains tax while supporting philanthropic goals:

- Donor-Advised Funds (DAFs): Donate appreciated assets, avoid paying capital gains tax, and receive an immediate charitable deduction.

- Charitable Remainder Trusts (CRTs): Transfer assets into a trust that provides income for a set period, with the remainder going to charity. Capital gains taxes are deferred and spread over time.

- Charitable Lead Annuity Trusts (CLATs): Provide annual payments to a charity for a set term, with the remainder returning to you or your heirs, potentially reducing estate and California capital gains tax exposure.

4. Installment Sales

Spreading the sale of a business, property, or large asset over multiple years through an installment sale allows you to spread out the California capital gains tax liability, keeping you in a lower tax bracket year over year.

5. Opportunity Zones

Investing in Qualified Opportunity Zones allows you to defer and reduce capital gains tax on a prior investment by reinvesting those gains into a Qualified Opportunity Fund. This can be a powerful tool for both federal and California capital gains tax planning. Long-term investors may eliminate taxes on new gains altogether.

6. Maximizing the Home Sale Exclusion

If you sell your primary residence, you may be eligible to exclude up to $250,000 (single) or $500,000 (married filing jointly) of capital gains from taxes, including California capital gains tax, provided you’ve lived in and owned the home for at least two of the last five years.

7. Using Retirement Accounts for Tax Deferral

Investing through tax-advantaged retirement accounts like IRAs or 401(k)s can defer taxes on capital gains until distribution. Roth IRAs offer the added benefit of tax-free qualified withdrawals, including gains, in retirement, helping you avoid both federal and California capital gains tax on those earnings.

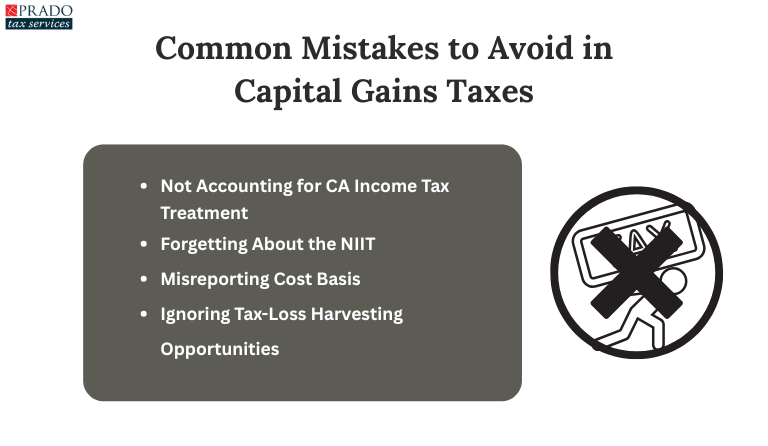

Common Mistakes to Avoid in Capital Gains Taxes

When dealing with capital gains taxes, it’s easy to make costly errors if you’re not fully aware of the rules and nuances, especially in California. Here are some common mistakes to watch out for:

1. Not Accounting for California’s Income Tax Treatment

Unlike federal rules that offer preferential rates on long-term capital gains, California taxes capital gains as regular income. Many taxpayers overlook this, leading to unexpectedly higher state tax bills. It’s essential to factor in California’s progressive income tax brackets when estimating your total tax liability.

2. Forgetting About the Net Investment Income Tax (NIIT)

High earners often overlook the 3.8% Net Investment Income Tax, which applies to individuals with modified adjusted gross income above certain thresholds ($200,000 for singles, $250,000 for married filing jointly). This surtax can significantly increase your overall tax burden on capital gains.

3. Misreporting Cost Basis

Incorrectly calculating or reporting the cost basis of your assets can lead to paying more tax than necessary, or even trigger an audit. Always keep accurate records of purchase prices, improvements, and reinvested dividends to ensure your gains are properly calculated.

4. Ignoring Tax-Loss Harvesting Opportunities Before Year-End

Failing to review your portfolio for potential losses before the tax year ends means missing chances to offset gains and reduce your taxable income. Proactively identifying and selling underperforming assets can provide valuable tax relief.

Conclusion

Effective capital gains tax planning is essential for minimizing your overall tax burden, especially in California, where capital gains are taxed as ordinary income. By leveraging strategies such as tax-loss harvesting, holding assets long-term, utilizing charitable contributions, and taking advantage of retirement accounts, you can significantly reduce the amount of tax owed on your investments.

Understanding both federal and state tax rules and how they interact is key to making informed decisions that protect your wealth. Being proactive, avoiding common mistakes, and staying current with potential tax law changes will further strengthen your financial position.

Consider working with a California-based tax consultant like Prado Tax Services, which provides personal and business tax services to tailor strategies to your specific situation. Contact us at Prado Tax Services today to navigate complex tax regulations and maximize your savings.